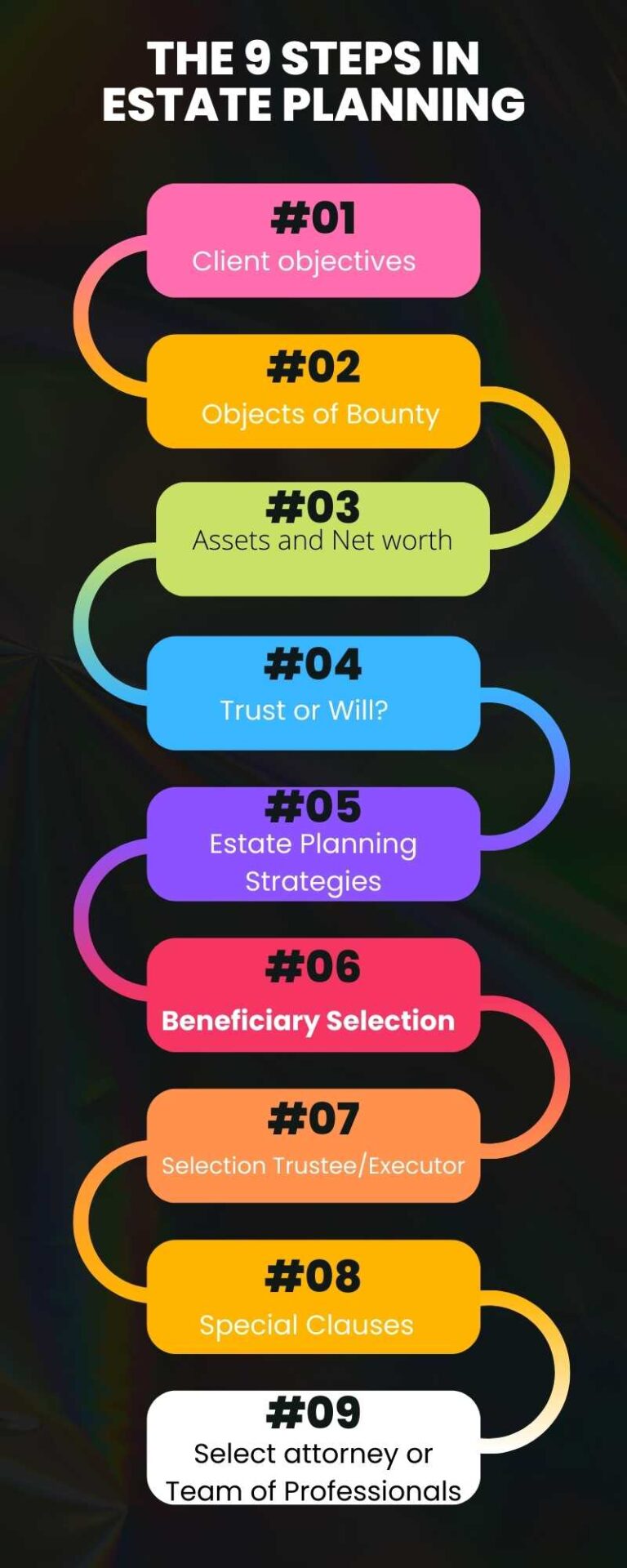

Step #4: Decide between a Trust or a Last Will and Testament.

An Estate Plan can use either a “simple Will” (Last Will and Testament) OR a Trust as the fundamental estate planning document. The decision between the two involves a number of considerations.

Step #5: Consider Estate Planning Strategies.

…… But what kind of Trust? There are many kinds of trusts. Each has different requirements and different strategic objectives. The point is not a list of different kinds of trusts, instead the point is to review which estate planning strategies align with your own objectives. Estate planning strategies naturally lead into different kinds of trust that can accomplish your own personal objectives.

Step #6: Decide who YOU want to be the Beneficiary.

Clients should consider both Primary beneficiaries and Secondary beneficiaries:

A) Selection of Primary Beneficiaries.

Successful Estate Planning involves “having happen what you want to have happen.” Each client decides what is right for their situation and their wishes.

Some clients name children equally, other clients do not choose to distribute equally. Some clients have no children, and choose particular charities as their beneficiaries. Some clients, similar to Warren Buffet and Bill Gates, have children but nevertheless select charities as their beneficiaries.

Some clients choose a friend for part or all of their estate.

Naturally, a spouse is often the first choice, but not always. Note that there are some limitations on your ability to disinherit a spouse; although, there is not requirement under Florida law to leave any portion of your estate or trust to your own children, grandchildren, or other relatives.

The bottom line is that it is your choice.

B) Selection of Secondary Beneficiaries.

It is a good idea to try to always have “contingent” or “secondary” beneficiaries. If your primary beneficiary predeceases you, you will then have the contingency covered in advance. The contingent beneficiary that you name can be the primary beneficiary’s descendants, the other primary beneficiaries, or some other person or charity entirely.

It is true that you could skip the naming of contingent beneficiaries, and only name them if the primary beneficiaries predecease.

However, there is a disadvantage to waiting. If the predecease happens when you are disabled, incompetent, or distracted, the necessary update may never be made.

If you name a contingent beneficiary now, there will be no extra expense, time or trouble, or any effort to later name the contingent beneficiary. And if you change your mind at a later date, when the primary beneficiary predeceases, you can always then do an amendment to your estate plan.